Global shocks, climate risks and economic realities reshape South Africa’s agricultural outlook

South Africa’s agricultural sector enters the next cycle against a backdrop of unusually elevated global uncertainty. While the industry has performed well in recent years, despite logistics constraints and biological risks, a convergence of geopolitical tensions, higher energy prices and climate risks is reshaping the outlook for producers, exporters and agribusinesses.

In a recent Coface webinar, Aroni Chaudhuri, Coface Chief Africa Economist, outlined how international developments are progressively filtering through to the agricultural sector, with pressures expected to intensify towards the end of 2026 and into 2027.

Global geopolitics: indirect but unavoidable pressure

Although agriculture is not the first sector to feel the immediate effects of the Middle East conflict, the current crisis is creating conditions that will eventually weigh on global agri‑food systems. The most immediate transmission channels are energy and fertilizers.

Disruptions to oil flows have resulted in an imbalance between global supply and demand, pushing prices higher and keeping them there. Unlike the previous shock on oil prices, where volatility was largely driven by risk sentiment, the current environment is characterized by actual physical shortages in oil markets. This distinction is critical for agriculture, a sector heavily exposed to fuel‑intensive production and transport.

Higher oil prices raise farming costs directly through mechanisation and logistics, and indirectly through inflation across the broader economy. For emerging markets such as South Africa, these price pressures are especially significant.

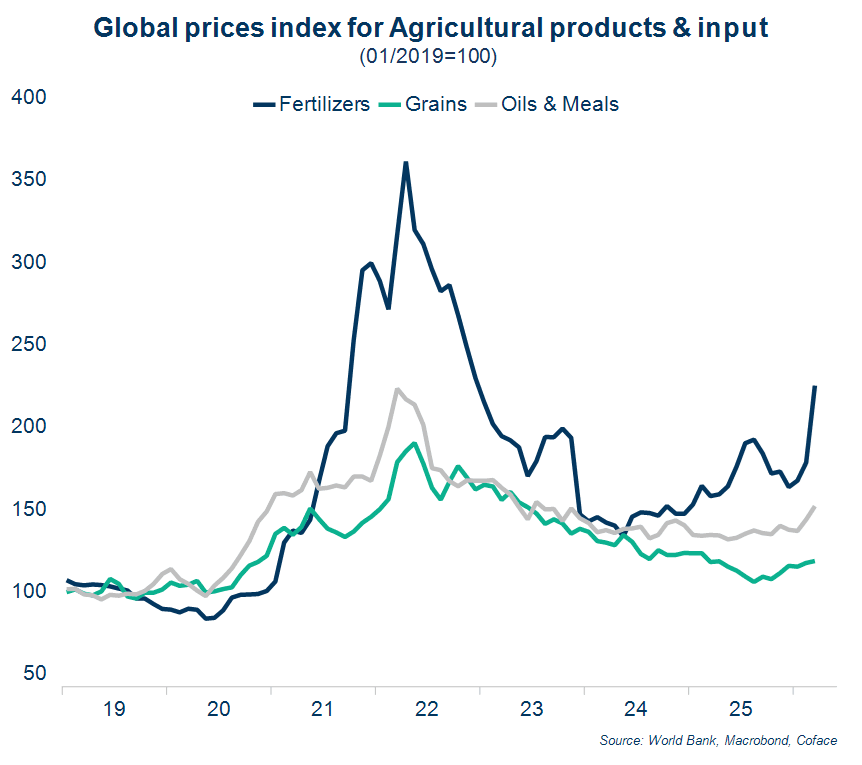

Rising input costs and fertilizer uncertainty

Rising input costs and fertilizer uncertainty

Beyond energy, disruptions to chemical supply chains are adding another layer of complexity. Fertilizer markets, while currently supported by existing inventories, are already experiencing upward price pressure. The risks here are less about immediate shortages and more about future accessibility and affordability, particularly once large importing nations return to the market to rebuild stocks.

For South African buyers, this creates uncertainty around input costs at a time when margins are already under pressure. Even modest fertilizer price increases can significantly affect cash flow, especially for smaller and mid‑sized operators within the agricultural value chain.

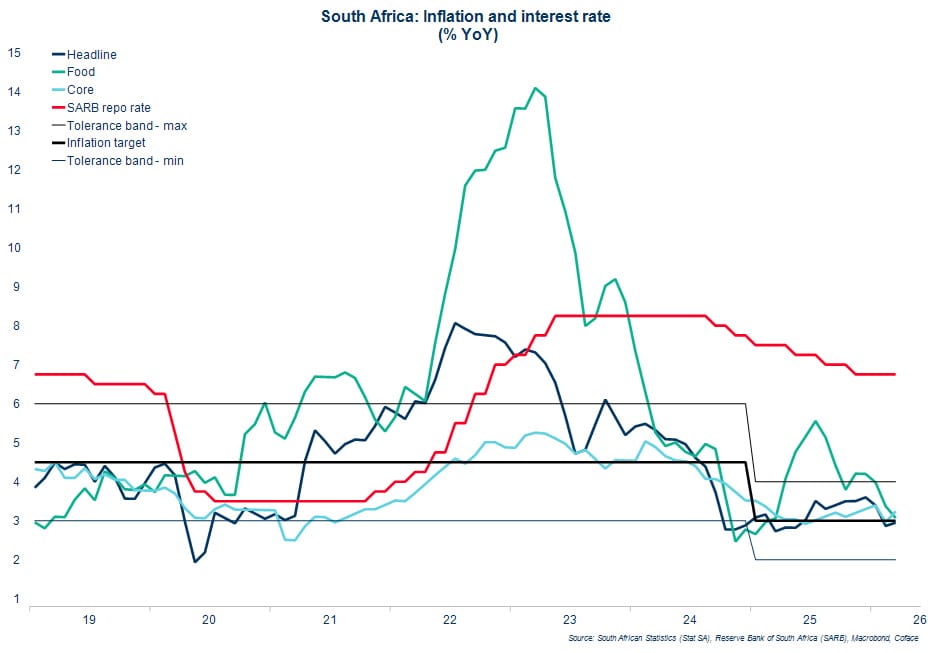

Why South Africa is vulnerable, but not exposed to immediate supply failure

South Africa’s vulnerability to global shocks is primarily price‑driven. As a net importer of refined petroleum products, the country remains highly sensitive to sustained increases in global oil prices. However, its level of income and market access should allow it to secure supply, albeit at higher cost.

The implications are macroeconomic. Higher fuel prices feed into inflation, particularly through transport, constraining the scope for monetary easing. Low inflation had been an important driver of growth momentum in South Africa, and renewed price pressure limits the ability of the Reserve Bank to support demand through monetary policy.

Tighter financial conditions mean that credit availability and borrowing costs are likely to remain elevated, affecting investment and working capital across the agricultural sector.

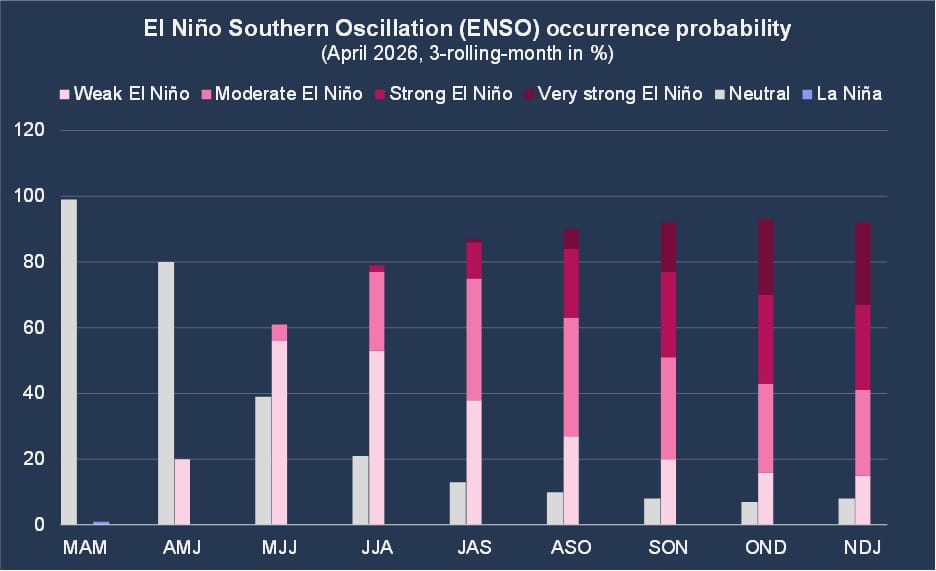

Climate risks: El Niño returns

Climate risks: El Niño returns

Layered on top of geopolitical and economic pressures is a familiar but major risk: El Niño. Forecasts point to a high probability of El Niño conditions re‑emerging later in 2026, bringing warmer and drier weather patterns to Southern Africa.

Historically, El Niño episodes have coincided with lower agricultural output in South Africa, particularly during the summer planting season. While current harvest expectations for 2026 remain favourable due to adequate rainfall in the past season, the outlook becomes more challenging beyond that.

The greatest risk lies in the possibility of a prolonged and/or intensified El Niño, which would deepen pressure on water availability, crop yields and overall production levels heading into 2027.

Diverging dynamics within agriculture

Not all subsectors are affected equally. Crop production has benefited from strong harvests in recent years, keeping cereal supplies ample and prices relatively subdued. Demand for cereals remains stable, driven primarily by demographic factors rather than cyclical swings.

The livestock sector, however, continues to face pressure from disease outbreaks, biosecurity concerns and rising feed costs. Combined with higher input prices, this divergence highlights the uneven nature of risk across the agricultural landscape.

Producer price inflation, which had eased prior to the geopolitical shock, is now likely to reverse. Rising fertiliser, fuel and intermediate input costs are expected to place renewed pressure on farm margins and profitability.

Resilience remains, but pressures are building

Despite these challenges, South African agriculture remains fundamentally resilient. Strong institutional frameworks, improving yields over time and access to capital among larger producers provide important buffers against external shocks.

However, the balance of risks has clearly shifted. The convergence of global conflict, higher financing costs and climate uncertainty introduces a more demanding operating environment, particularly towards the end of 2026 and into 2027.

The key challenge for the sector is no longer simply growth, but managing volatility, protecting cash flow and navigating risk across increasingly complex value chains. In this context, economic insight, scenario planning and proactive credit risk management become essential tools for sustaining performance in an uncertain global landscape.